Finova.tech Review: A Critical Examination of the “Powering UK Lending” Platform

Table of Contents

Introduction: Analyzing the Finova.tech Proposition

In the dynamic world of financial technology, platforms that promise to revolutionize established industries demand close scrutiny. Finova.tech makes a bold entry with a grand claim: “Powering the UK’s lending market faster, smarter, and more connected.” The platform’s marketing presents staggering figures and a comprehensive suite of services aimed at major lenders. This Finova.tech review provides a critical, evidence-based analysis of the platform’s claims, transparency, and overall credibility. Our goal is to determine whether this fintech platform stands as a legitimate innovator or presents an example of overreach in the UK lending market.

First Impressions and Scale of Claims

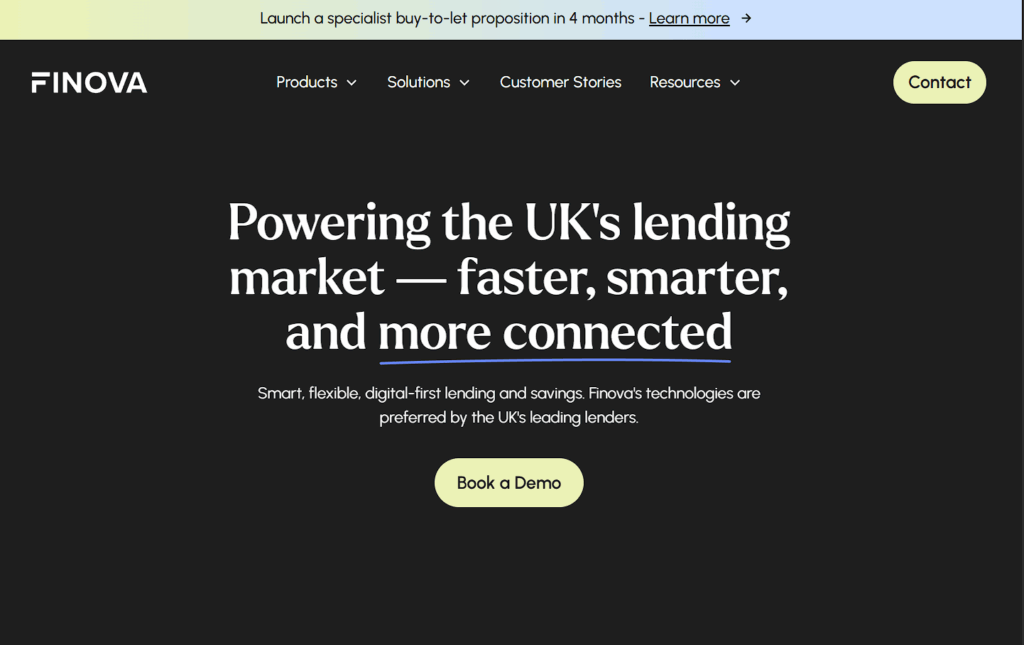

The Finova.tech website is professionally designed, using a modern, corporate aesthetic common in B2B financial software. It immediately asserts an enormous scale of operation, stating it has overseen “Over £500 billion originated” and manages “£47.5 billion under management” for “1000+ happy clients.” These numbers are designed to create instant authority and position the Finova.tech platform as a dominant, systemically important player in UK finance.

For any institution evaluating a core technology partner, these figures would be highly compelling. The website further details a broad product portfolio covering Lending, Savings, Servicing, Decisioning, Intermediary Management, and Broker Payments. It claims to serve every segment of the market, from high-street banks and building societies to specialist lenders and brokers. However, this powerful first impression is precisely why a deeper, more skeptical analysis is essential. The initial polish must be weighed against verifiable substance.

Critical Analysis: Unverifiable Claims and Corporate Opacity

The most significant red flags for the Finova.tech platform relate to the verifiability of its extraordinary claims and a near-total lack of corporate transparency.

1. The Problem of Unsubstantiated Scale:

The figures of £500+ billion and £47.5 billion are not just impressive; they are colossal. To put this in context, it would represent a substantial portion of the entire UK mortgage market. A company legitimately operating at this scale would be a household name in financial circles, with extensive media coverage, clear regulatory footprints, and publicly named flagship clients. However, Finova.tech provides no external evidence to support these numbers.

There are no named client case studies from the “UK’s leading lenders” it claims to serve. There are no links to audited financial reports, regulatory filings, or independent press releases confirming partnerships. The claims exist solely within the platform’s own marketing ecosystem, a classic tactic known as “proof by assertion.” In the fintech industry, trust is built on demonstrable proof and third-party validation, not on self-reported statistics.

2. Complete Anonymity and Missing History:

A legitimate financial technology provider, especially one handling sensitive data and transactions for regulated institutions, is transparent about its identity. The Finova.tech website reveals a profound lack of basic corporate information.

- No Legal Identity: The platform does not clearly state its registered legal company name (e.g., Finova Ltd.) or its Company Registration Number from UK Companies House.

- No Leadership Team: There are no named founders, directors, or an executive team with professional biographies.

- No Verifiable History: There is no “About Us” narrative explaining the company’s founding, growth timeline, or major milestones. How did it achieve this purported scale? The story is missing.

- Ambiguous Testimonials: Client quotes are generic and anonymous (e.g., “Finova has been nothing short of transformational”), lacking the specific names and positions that would allow for verification.

This corporate opacity makes it impossible for a potential client or partner to perform basic due diligence. Who is ultimately responsible for the platform’s operations and the financial data it claims to manage? The silence on these fundamental points is a severe credibility issue.

Product Portfolio and the “One-Stop-Shop” Paradox

Finova.tech markets itself as a comprehensive, all-in-one solution. While an integrated platform is a valid model, the claimed expertise across such distinct and complex areas from core lending origination and sophisticated risk decisioning to savings account management and broker payment systems is extraordinary.

Each of these verticals requires deep, specialized regulatory knowledge and technical investment. Established fintech leaders typically excel in one niche before expanding. The claim of best-in-class capability across the entire spectrum simultaneously, without a visible history of specialization or verifiable client references in each area, stretches credulity. It can indicate a “jack of all trades” approach that may lack the depth required by serious financial institutions.

The “Broker Payments” Scheme: A Notable Incentive

One product offering particularly stands out: “Broker Payments: Earn more money for the same work. Get 50% profit share on top of your proc fees, paid quarterly.“

This is an unusually aggressive commercial offer. In standard finance, brokers earn commissions. A “50% profit share” suggests a deep financial entanglement that is unconventional for a technology provider. Such high-incentive models can act as a powerful lure but require absolute transparency on profit calculation a transparency absent from the site. This type of offer warrants extreme caution and thorough investigation.

The Crucial Context of UK Financial Regulation

Finova.tech explicitly targets the UK lending market, one of the world’s most stringently regulated environments under the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The Glaring Regulatory Silence:

Any platform “powering” UK lenders and handling consumer financial data must demonstrate rigorous compliance with FCA rules on data security, consumer duty, and financial promotions. It is standard, non-negotiable practice for a legitimate provider to prominently display its regulatory status, FCA authorization numbers, or key certifications like ISO 27001 for information security.

The Finova.tech website contains no mention of FCA authorization, registration, or any compliance certifications. This omission is not a minor oversight; for a firm claiming to serve UK banks, it is a fundamental and alarming red flag. It suggests either a lack of understanding of the market’s basic requirements or an intentional decision to operate outside the regulatory framework a completely untenable position for a genuine B2B financial services provider.

A Comparative Overview: Finova.tech vs. a Legitimate Fintech Provider

| Feature | A Legitimate, Established Fintech Provider | Finova.tech (Analysis) |

|---|---|---|

| Scale Claims | Supported by named client case studies, press releases, and verifiable industry reports. | Presents unverifiable, colossal figures (£500bn+) with no external evidence or named clients. |

| Corporate Transparency | Clear legal entity, Companies House number, named leadership team, and published company history. | Complete opacity. No legal name, no leadership team, no verifiable history or physical address. |

| Regulatory Compliance | Prominently displays FCA authorization, regulatory registrations, and security certifications (e.g., ISO 27001). | No mention of FCA status or any compliance certifications. Operates in a stated regulatory vacuum. |

| Client Validation | Website features logos of named banking/lending partners and detailed, attributable testimonials. | Relies on anonymous, generic testimonials. No logos or names of the “leading lenders” claimed as clients. |

| Product Depth | Often a proven expert in one or two core areas before expanding, with deep documentation. | Claims expert-level, all-in-one capability across six+ complex areas with no proven specialization. |

Essential Due Diligence for Financial Institutions

Before any engagement with a platform like Finova.tech, rigorous, independent verification is mandatory:

- Verify the Corporate Entity: Demand the full legal company name and UK Companies House registration number. Search this information independently on the official Companies House register.

- Confirm Regulatory Status: Ask for specific FCA authorization numbers. Verify them directly on the FCA’s Financial Services Register. The absence of a listing is an absolute deal-breaker.

- Request Client References: Ask for contact information for at least two existing clients in your sector (e.g., a named building society or specialist lender). Speak to them directly about their implementation and experience.

- Audit the Technology: For a core platform, insist on a detailed technical architecture review, security audit reports, and data residency assurances. A legitimate provider will have this documentation.

- Scrutinize Contracts: Have all proposed agreements reviewed by specialized financial services legal counsel, paying close attention to liability clauses, data ownership, and service level agreements (SLAs).

Report Finova.tech and Recover Your Funds

If you have suffered financial loss due to Finova tech or a similar scam, it is crucial to take immediate action. Report the incident to SPS Investigation Ltd, a reputable organization committed to assisting victims in recovering their stolen assets. Acting promptly can significantly improve the chances of reclaiming funds and preventing further fraudulent activity.

Conclusion: Final Verdict on Finova.tech

This Finova.tech review concludes that the platform exhibits multiple characteristics of a high-risk, unverifiable operation. The combination of unsubstantiated astronomical claims, complete corporate anonymity, and a glaring lack of regulatory disclosure creates an unacceptable risk profile for any serious financial institution.

While the website successfully creates an image of scale and capability, it fails to provide the foundational pillars of trust required in the fintech industry: transparency, verifiable proof, and regulatory compliance. The platform’s narrative is built on assertions that cannot be checked, from unnamed clients to an invisible corporate structure.

Ever had an encounter with Finova.tech or a similar platform? Contribute your insights in the comments section or seek guidance on prudent investment strategies. Remain vigilant and prioritize personal security at all times when navigating the digital financial landscape.